Thursday, 17 December, 2026 - 08:30 to 20:00 Paris time

Pullman Paris Montparnasse Hotel - PARIS, FRANCE

Presentation

The EUROFIDAI-ESSEC Paris December Finance Meeting will hold its 24th edition in-person in downtown Paris (Pullman Paris Montparnasse Hotel) on December 17, 2026.

The conference is organized by EUROFIDAI (European Financial Data Institute) and the ESSEC Business School and jointly sponsored by Amundi / PLADIFES / CERESSEC / CDC Institute for Economic Research / Clipway.

All researchers are invited to present in English their latest research in all areas of finance. Job market papers are welcomed and integrated in normal sessions. They will be highlighted in the program.

In recent years, the conference has become very selective with one in six submitted papers accepted. The EUROFIDAI-ESSEC Paris December Finance Meeting is ranked 2nd in Europe and 8th in the World among large conferences based on papers published in the Top3 Finance and Top5 Economics journals - "Ranking Finance Conferences: An Update Conferences: An Update" by W. Hou, E. Smajlbegovic and D. Urban, J. of Empirical Finance, 84 (2025).

Prizes will be awarded for the Best Conference Paper and the Best Job Market Paper.

Timeline

- Submissions opening: April 7, 2026

- Submissions deadline: May 31, 2026

- Notice of acceptance:June 30, 2026 - PLEASE EXPECT SOME DELAY. ALL NOTICES WILL BE SENT BY THE END OF JULY.

- Registration deadline for accepted authors: July 15, 2026

- Online Program: September, 2026

- Registration deadline for other participants: November 29, 2026

Our sponsors

Submissions opening: April 7, 2026

Submissions deadline: May 31, 2026

The EUROFIDAI-ESSEC Paris December Finance Meeting will hold its 24th edition in-person in downtown Paris (Pullman Paris Montparnasse Hotel) on December 17, 2026.

The conference is organized by EUROFIDAI (European Financial Data Institute) and the ESSEC Business School and jointly sponsored by Amundi / PLADIFES / CERESSEC / CDC Institute for Economic Research / Clipway.

All researchers are invited to present in English their latest research in all areas of finance. Job market papers are welcomed and integrated in normal sessions. They will be highlighted in the program.

In recent years, the conference has become very selective with one in six submitted papers accepted. The EUROFIDAI-ESSEC Paris December Finance Meeting is ranked 2nd in Europe and 8th in the World among large conferences based on papers published in the Top3 Finance and Top5 Economics journals - "Ranking Finance Conferences: An Update Conferences: An Update" by W. Hou, E. Smajlbegovic and D. Urban, J. of Empirical Finance, 84 (2025).

Prizes will be awarded for the Best Conference Paper and the Best Job Market Paper.

Submission process

Submissions open on April 7, 2026

Only on-line submissions will be considered. Before filling the application form, authors should read the following instructions.

Prepare 2 files in pdf format:

- An anonymous version of the paper (the complete paper without the name(s) of the author(s), the acknowledgements and any indication of author’s affiliation)

- A complete version of the paper including the following information: title, name(s) of the author(s), abstract, keywords, email address for each author, complete address(es)

- The abstract to be filled with the submission form should not exceed 150 words.

Keywords

To complete their submission, authors are asked to classify their paper using 3 keywords (all fields of finance).

Submission fees

The submission fee for each paper is 75€ and non-refundable. Submitting authors will receive a receipt following completion of the submission process.

Authors

Due to the high number of submissions, one author can submit multiple papers (joint or single-authored) but cannot have more than one paper accepted.

Paper diffusion

Accepted papers will be posted on the website of the conference.

Co-Presidents of the Scientific committee

- Jocelyn Martel - ESSEC Business School

- Elise Gourier - ESSEC Business School

2026 Scientific committee

- Yacine Ait-Sahalia - Princeton University

- Patrick Akey - ESSEC Business School

- Nihat Aktas - WHU Otto Beisheim School of Management

- Patrick Augustin - McGill University

- Laurent Bach - ESSEC Business School

- Vimal Balasubramaniam - Queen Mary University

- Daniele Bianchi - Queen Mary University

- Maxime Bonelli - London Business School

- Romain Boulland - ESSEC Business School

- Marie-Hélène Broihanne - Université de Strasbourg

- Georgy Chabakauri - London School of Economics

- Jean-Edouard Colliard - HEC Paris

- Pierre Collin-Dufresne - EPFL

- Ettore Croci - Universita Cattolica del Sacro Cuore

- Serge Darolles - University Paris-Dauphine

- Matt Darst - Board of Governors of the Federal Reserve

- Laurence Daures - ESSEC Business School

- François Degeorge - University of Lugano

- Catherine D'Hondt - UC Louvain

- Alberta Di Giuli - ESCP Europe

- Philippe Dupuy - EM Grenoble

- Matthias Efing - HEC Paris

- Ruediger Fahlenbrach - EPFL & SFI

- Félix Fattinger - WU Vienna University of Economic and Business

- Andras Fulop - ESSEC Business School

- Jean-François Gajewski - IAE Lyon

- Emilia Garcia-Appendini - University of St-Gallen

- Edith Ginglinger- Université Paris-Dauphine

- Elise Gourier - ESSEC Business School

- Peter Gruber - Università della Svizzera Italiana

- Alex Guembel - Toulouse School of Economics

- Ulrich Hege - Toulouse School of Economics

- Georges Hübner - HEC Liège

- Julien Hugonnier - EPFL

- Heiko Jacobs - University of Duisburg-Essen

- Sonia Jimenez - Grenoble INP

- Alexandros Kostakis - University of Liverpool

- Dmitry Kuvshinov - Universitat Pompeu Fabra

- Jongsub Lee - Seoul National University

- Junye Li - Fudan University

- Abraham Lioui - EDHEC

- Elisa Luciano - Collegio Carlo Alberto

- Victor Lyonnet - University of Michigan

- Yannick Malevergne - Université de Paris 1 Panthéon-Sorbonne

- Roberto Marfé - Collegio Carlo Alberto

- Jocelyn Martel - ESSEC Business School

- Maxime Merli - Université de Strasbourg

- Roxana Mihet - Lausanne University

- Sophie Moinas - Toulouse School of Economics

- Lorenzo Naranjo - Washington University in Saint-Louis

- Lars Norden - EBAPE/FVG

- Clemens Otto - Singapore Management University

- Loriana Pelizzon - Goethe University

- Fabricio Perez - Wilfrid Laurier University

- Christophe Pérignon - HEC Paris

- Joël Petey - Université de Strasbourg

- Ludovic Phalippou - Oxford University

- Alberto Plazzi - University of Lugano & SFI

- Sébastien Pouget - Toulouse School of Economics

- Vesa Pursiainen - University of St. Gallen

- Sofia Ramos - ESSEC Business Schooll

- Jean-Paul Renne - HEC Lausanne

- Michel Robe - Robins School of Business, University of Richmond

- Tristan Roger - ICN

- Jeroen Rombouts - ESSEC Business School

- Guillaume Roussellet - McGill University

- Julien Sauvagnat - Bocconi University

- Olivier Scaillet - University of Geneva & SFI

- Paolo Sodini - Stockholm School of Economics

- Christophe Spaenjers - University of Colorado Boulder

- Ariane Szafarz - University Libre de Bruxelles

- Peter Tankov - ENSAE Paris

- Roméo Tédongap - ESSEC Business School

- Erik Theissen - University of Mannheim

- Micheal Troege - ESCP Europe

- Boris Vallée - INSEAD

- Philip Valta - University of Bern

- Guillaume Vuillemey - HEC Paris

- Rafal Wojakowski - Surrey Business School

- Alminas Zaldokas - NUS

- Frederica Zeni - EPFL

- Olivier-David Zerbib - ENSAE Paris

- Marius Zoican - University of Calgary

Click here to access the registration form

Registration fees

- Presenting authors : 275€

- Chairs : 125€

- Discussants : 125€

- Phds (not presenting) : 75€

- Other participants : 275€

Accepted Job market papers visible in this section from October, 2026.

To provide job market candidates with more visibility, Job Market papers will be highlighted in the conference program and in this section. Although job market papers are inserted in normal sessions, they will be considered for a separate prize, the Best Job Market Paper Award.

Every year, we reward the Best Conference Paper and the Best Job Market Paper.

Find below all awarded papers.

2025

Best Conference Paper Award:

- "How do households suppress the price of tail risk?" by Laurent Calvet (SKEMA Business School), Claire Celerier (University of Toronto - Rotman School of Management), Gordon Y. Liao (Circle) and Boris Vallee, PhD, CFA (INSEAD)

Best Job Market Paper Award:

- "Short-Termis Carbon Emissions" by Kai Mäckle (University of Mannheim)

Best Paper Using EUROFIDAI Data Award (using EUROFIDAI High Frequency data):

"Click First or Last? Strategic Order Submission During the Euronext Preopening Session" by Laurence Daures (ESSEC Business School), Sophie Moinas (Toulouse School of Economics), Selma Boussetta (Université de Bordeaux), published in Management Science (2025)

2024

Best Paper Conference meeting:

- Ulrich HEGE (Toulouse School of Economics), Kai LI (Peking University) and Yifei ZHANG (Peking University), for the paper entitled "Climate Innovation and Carbon Emissions: Evidence from Supply Chain Networks"

Best Job Market Paper meeting:

- Alessio OZANNE (Toulouse School of Economics), for the paper entitled “Black Box Credit Scoring and Data Sharing”

2023

Best Paper Conference meeting:

- "Andras FULOP (ESSEC), Junye LI (Fudan University) and Mo WANG (ESSEC), for the paper entitled "Option Mispricing and Alpha Portfolios"

Best Job Market Paper meeting:

- Antoine BAENA (Banque de France and Paris Dauphine University PSL, France), for the paper entitled "Do capital requirements really reduce the riskiness of banks"

2022

- Victor LYONNET (Ohio State University) & Lea STERN (University of Washington) for the paper entitled "Venture Capital (Mis)Allocation in the Age of AI"

2021

- Dmitry KUVSHINOV (University of Pompeu Fabra) for the paper entitled "The Co Movement Puzzle"

2020

- Olivier David ZERBIB (Tilburg University (CentER) and ISFA) for the paper entitled "A Sustainable Capital Asset Pricing Model (S CAPM): Evidence from Green Investing and Sin Stock Exclusion"

2019

- Matthias EFING (HEC Paris), Harald HAU (University of Geneva & Swiss Finance Institute), Patrick KAMPKOTTER (University of Tübingen) and Jean-Charles ROCHET (University of Geneva & Swiss Finance Institute) for the paper entitled "Bank Bonus Pay as a Risk Sharing Contract"

2018

- Ye LI & Chen WANG for the paper entitled "Rediscover Predictibility: Information from the Relative Prices of Long-Term and Short-Term Dividends"

2017

- Thorsten MARTIN & Clemens A. OTTO for the paper entitled "The Effect of Hold-Up Problems on Corporate Investment: Evidence from Import Tariff Reductions"

2016

- Matthew DARST & Ehraz REFAYET for the paper entitled "Credit Default Swaps in General Equilibrium: Spillovers, Credit Spreads, and Endogenous Default"

2015

- Roberto MARFE for the paper entitled "Labor Rigidity and the Dynamics of the Value Premium"

2014

- Taylor BEGLEY for the paper entitled "The Real Costs of Corporate Credit Ratings"

- Shiyang HUANG for the paper entitled "The Effect of Options on Information Acquisition and Asset Pricing"

2013

- Clemens OTTO & Paolo VOLPIN for the paper entitled "Marking to Market and Inefficient Investment Decisions"

- Matthias EFING & Harald HAU for the paper entitled "Structured Debt Ratings: Evidence on Conflicts of Interest"

- Bart YUESHEN for the paper entitled "Queuing Uncertainty"

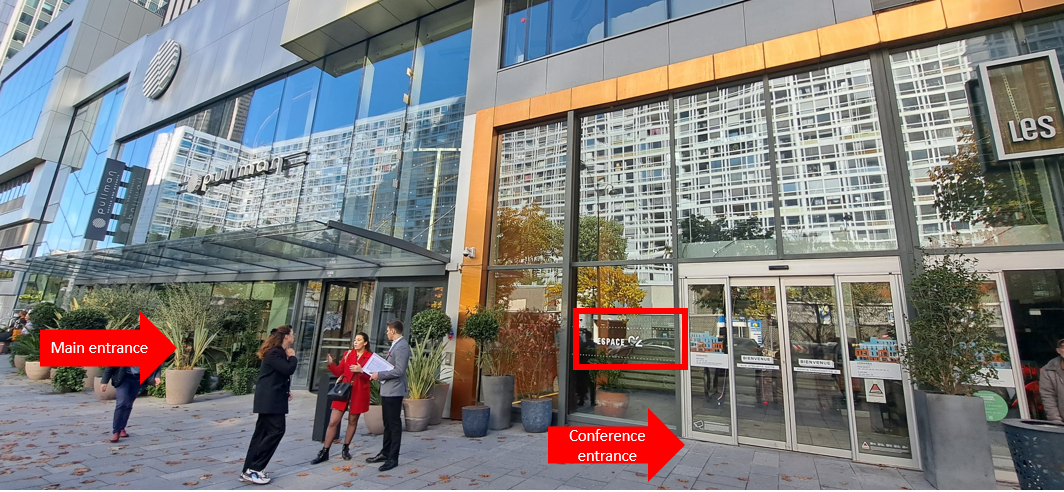

Location

PULLMAN PARIS MONTPARNASSE HOTEL

19 rue Commandant René Mouchotte, 75014 Paris

Special rate for participants

After your registration, if you want to get a special rate at the PULLMAN PARIS MONTPARNASSE hotel (280€ / night, including breakfast) please contact the organizing committee: conference[at]paris-december.eu.

Deadline November 16, 2026 - Within the limit of available rooms

Access

Public transportation:

Subway | Gaité (300m - 0.18 miles ) - line 13

Subway | Montparnasse Bienvenüe (200m - 0.12 miles) - line 4, 6, 12, 13

Bus | Montparnasse Bienvenüe (500m - 0.31 miles) - line 28, 39, 58, 91, 92, 94, 95, 96

Train Station | Montparnasse train station (200m - 0.12 miles)

From Roissy airport:

Public transportation | RER B and metro lines 4 or 6 (stop at Montparnasse-Bienvenüe)

From Orly airport:

Public transportation | OrlyBus to Denfert-Rochereau and metro line 6 (stop at Montparnasse-Bienvenüe)

By car: